When planning for retirement, one of the most important decisions you will make is whether to manage your own investments or work with a financial adviser.

Managing your own retirement investments can offer lower costs, but many investors underperform due to behavioural mistakes and inconsistent decision-making. In contrast, working with a financial adviser can provide structure, discipline and long-term planning, helping you stay on track and avoid costly errors.

The approach you choose can have a significant impact on your long-term outcomes, not just in terms of returns, but also in how consistently you stick to your plan.

In this article, we explore the differences between managing your own investments and working with a financial adviser, and how each approach can impact your long-term retirement outcomes.

Managing your own retirement portfolio

Managing your own retirement investments can offer greater control and lower costs, but it also requires discipline, consistency, and the ability to make rational decisions during market volatility.

The rise of online platforms, low-cost funds, and readily available financial information has made it easier than ever for individuals to manage their own investments.

On the surface, this approach offers several clear advantages:

- Full control over investment decisions

- Lower costs, as you avoid advisory fees

- Flexibility to adapt your strategy at any time

For disciplined and experienced investors, this can be an effective route. However, the key word here is disciplined.

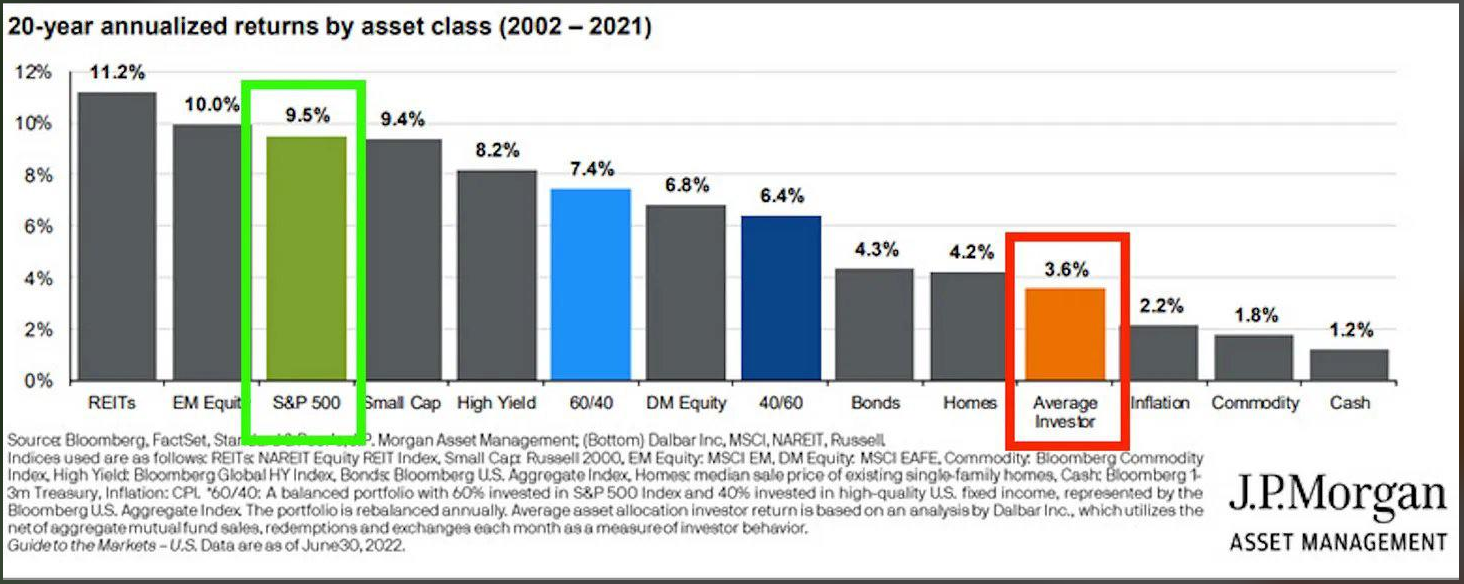

Figure 1: Average US Investor vs S&P 500 Returns (2002–2021)

Illustrates the gap between average US investor returns (~3.6%) and the S&P 500 (~9.5%).

Why investor behaviour is the biggest risk to your investments

While markets themselves can be volatile, the evidence consistently shows (as seen in figure 1) that investor behaviour is often the primary cause of underperformance.

Research such as DALBAR’s Quantitative Analysis of Investor Behaviour highlights a persistent gap between market returns and the returns actually achieved by investors. This gap is largely driven by poor decision-making at the wrong times.

Common behavioural pitfalls include:

- Buying after strong performance: Investors are naturally drawn to what has recently done well, often entering markets after prices have already risen.

- Selling during downturns: Fear during market declines leads many investors to sell at the worst possible time, locking in losses.

- Switching strategies too frequently: Constantly changing funds or approaches in response to short-term performance rarely leads to better outcomes.

- Overconfidence: Many investors believe they can outperform the market, despite overwhelming evidence showing how difficult this is to achieve consistently.

These behaviours can significantly reduce long-term returns, even if the underlying investments themselves are sound.

The Risks of Trying to Time the Market

A particularly damaging form of poor investor behaviour is attempting to time the market.

Many investors believe they can avoid losses by moving into cash during downturns and reinvesting when conditions improve. While this approach is appealing in theory, the evidence shows it is extremely difficult to execute successfully.

Research analysing the S&P 500, including data highlighted by Advisorpedia using J.P. Morgan Asset Management figures, demonstrates just how costly this behaviour can be.

Looking at a $10,000 investment over a 20-year period:

- Fully invested: grows to approximately $64,000+

- Miss the 10 best days: falls to around $29,000

- Miss the 20 best days: drops further to roughly $17,000

- Miss the 50 best days: declines to just $5,700

In other words, missing just a handful of days can cut your total return by more than half, and missing more can almost completely erode long-term growth.

This happens because market returns are not evenly distributed. A significant portion of gains comes from a very small number of days, and crucially, these days are unpredictable.

Even more importantly, the data shows that:

- The best days often occur very close to the worst days

- In many cases, the strongest rebounds happen immediately after sharp declines

- Some of the best days occur within days, or even the next day, after the worst days

This creates a major problem for investors trying to time the market.

If you sell after markets fall, which is the natural emotional response, you are highly likely to miss the recovery that follows.

As a result, market timing often leads to the exact opposite of what investors intend:

- Selling low

- Missing the rebound

- Re-entering at higher prices

This reinforces a key investment principle:

Time in the market is far more important than timing the market.

Remaining invested ensures you capture these critical periods of strong performance and benefit from compounding over time. Attempting to move in and out of the market, on the other hand, introduces a significant risk of being absent at exactly the wrong moments, ultimately reducing long-term returns.

The Discipline Challenge

Successful self-management requires more than knowledge. It requires:

- A clearly defined long-term strategy

- The ability to ignore short-term noise

- Emotional resilience during market volatility

- Consistent rebalancing and risk management

In practice, maintaining this level of discipline over decades, especially during market crises is extremely challenging.

Working with a Financial Adviser

Working with a financial adviser introduces a different approach, one that focuses not just on investments, but on the overall structure and sustainability of your financial plan.

What a Good Financial Adviser Actually Does

There is a common misconception that advisers simply “pick funds” or try to beat the market. In reality, their value is much broader.

A good adviser will:

- Create a tailored investment strategy: Built around your goals, time horizon, income needs, and risk tolerance.

- Provide behavioural coaching: Helping you stay invested during downturns and avoid emotionally driven decisions.

- Ensure proper diversification and risk management: Reducing exposure to unnecessary risks.

- Adapt your plan over time: As your life circumstances and market conditions change.

- Plan for retirement income: Including sustainable withdrawal strategies and sequencing risk.

- Optimise tax efficiency and estate planning: Ensuring your wealth is structured effectively for the long term.

In this sense, professional management is not just about investments, it is about decision-making, structure, and long-term discipline.

The Value of Financial Advice

One of the most widely cited studies in this area is Vanguard’s Advisor’s Alpha, which estimates that working with a financial adviser can add approximately 3% per year in net value.

Importantly, this value does not primarily come from outperforming the market. Instead, it comes from:

- Avoiding costly behavioural mistakes

- Maintaining a consistent long-term strategy

- Rebalancing portfolios effectively

- Implementing tax-efficient decisions

- Structuring withdrawals in retirement

Over time, even small improvements in these areas can compound into a significant difference in outcomes.

The Cost vs Value of Financial Advice

A common concern with professional advice is cost.

While it is true that advisers charge fees, it is important to consider this in the context of net outcomes rather than headline costs.

- Managing investments yourself may reduce fees, but increases the risk of poor decisions

- Professional advice introduces a cost, but may improve discipline and long-term returns

The key question is not simply:

“What does this cost?”

But rather:

“What is the net impact on my long-term financial outcome?”

DIY Investing or Working with an Adviser - Which is Best for You?

Choosing between managing your own investments and working with a financial adviser depends on your experience, discipline, and ability to stay committed to a long-term retirement strategy.

There is no one-size-fits-all answer. The right approach depends on your personality, experience, and ability to remain disciplined over time.

Managing your own investments may be suitable if you:

- Have strong investment knowledge

- Are emotionally disciplined during market volatility

- Can commit to a long-term strategy without deviation

- Are comfortable making complex financial decisions independently

Professional management may be more suitable if you:

- Prefer structure and guidance

- Want to avoid emotional decision-making

- Have complex financial needs (e.g. retirement income planning, tax considerations)

- Value having an experienced professional to guide long-term decisions

Final Thoughts

Long-term investment success is rarely about finding the perfect fund or timing the market correctly.

More often, it comes down to:

- Consistency

- Discipline

- Avoiding major mistakes

Managing your own investments can work well if you have the knowledge and temperament to stay the course through all market conditions.

However, many investors underestimate how difficult this is in practice.

For those individuals, working with a professional can provide not just expertise, but also the structure and behavioural support needed to stay on track - particularly during periods of uncertainty.

Ultimately, the best approach is the one that allows you to stick with your plan over the long term, because consistency, not complexity, is what drives results.

If this article really speaks to you and you value getting your investments and pensions working harder for you, please contact one of our advisers at Two10 Investment Services and we can talk through whether getting professional help makes sense for your situation.

At Two10 Investment Services, we support clients across Longridge, Preston and the Ribble Valley with tailored investment and retirement planning, offering complimentary consultations for those looking to discuss their investment strategy and long-term financial planning.

So please get in touch if you want to achieve your financial goals.

.jpg)

.png)

.png)

.png)